Check MEPCO Bill Online 2026 | See & Download Duplicate Bills

See Your MEPCO Bill Online

Every month, millions of households across Multan, Bahawalpur, Dera Ghazi Khan, Sahiwal, and other districts served by Multan Electric Power Company wait anxiously for their electricity bill, often unsure of the exact amount until the paper bill physically arrives. This delay leaves consumers unable to plan their monthly budget, track unusual spikes in unit consumption, or catch billing errors before the due date passes, sometimes resulting in late payment surcharges or even disconnection notices. With MeetYourBills, you can check your MEPCO bill online instantly using just your 14-digit reference number or 10-digit consumer ID, view your complete consumption history, and download a duplicate bill in seconds — no waiting, no registration, no confusion.

How to Check MEPCO Bill Online

Checking your mepco bill is quite simple and easy, it does not require you to sign in or register an account and its completely free. You just need to follow these steps to see your electricity bill.

Enter your 14 digit reference number in the search bar above

View Your Complete Bill

Click the “Check MEPCO Bill “ button

Download or Print

Wait for a few seconds to load your bill and download it

What is a Duplicate MEPCO Bill?

There comes a time when you loose printed bills from the MEPCO either it could be thrown in bins or kept somewhere safe but forgotten. In these alarming times, when the due date is reaching and you have no idea what my consumed units, charges, taxes, payable amount and due date would be. In those moments, duplicating your bills comes in handy, no need of paying a visit to the nearest MEPCO office or waiting for the mail to deliver your bill and following the above mentioned steps to check your MEPCO bill online, duplicating and downloading it makes your life very easy. Additionally, duplicate bills are digital copy of your electricity bill which can be stored in mobile or computer in a pdf format to track your electricity bill record and can be printed in times when you need them the most.

Checking MEPCO Online bill entering 14-Digit Reference Number

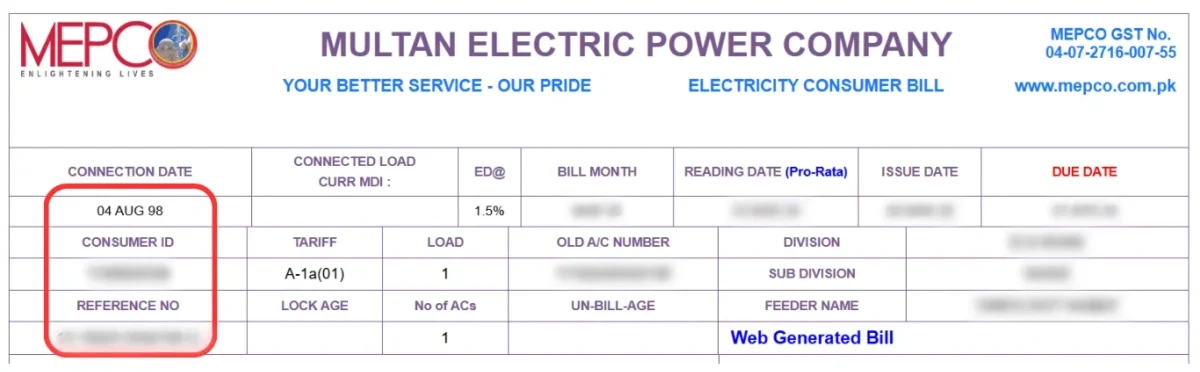

You know duplicating your bill is easy but what hurts the most when you cannot find your reference number. So, what is a reference number? A reference number is unique identifier number printed on your bill that is saved in the MEPCO database to track your bills. In the picture below, you can easily identify what it would look like in many cases. You can also read the full detailed guide about 14-digit reference number and how to find it.

How to Find Your MEPCO Reference Number Without an Old Bill

If you have read the full guide previously and still cannot find it, it could be mostly in those scenarios when you don’t have an old bill to look into. So, what needs to be done in moments like these? It’s a multi step process:

we need to find the reference number using CNIC

- Go to the official MEPCO site

- Look for CNIC registration option

- Type in your CNIC number

- Press search and you will find your 14- digit reference number

MEPCO SMS Service

check your mepco bill by writing “pitc 14-Digit reference number” and sending it to 8334.

MEPCO Mobile App

You can also download Roshan Mobile app from Playstore to find your mepco electricity bill.

Checking Through Banking apps

You can easily Check your electricity bills through JazzCash, Easypaisa and other banking apps.

MEPCO Bill Check by Customer ID

Until now we have discussed checking your bill using reference number, but what if there is another method to check your bill. That method is also similar like the previous one just the name is different this is called Customer ID which involves 10 digits. Just like reference number this is also printed on your bill you can find it in the highlighted section below. Infact, it is a personal choice how do you want to see your bill.

Check MEPCO Bill Via SMS

All previous methods involved internet and also web bill either it was checking your bijli bill on mobile or computer involved. But what if you don’t have an internet connection, cannot connect to the internet and in your mind due date, consumed units and payable amount are revolving around. That’s when SMS comes in handy, a long lost conventional technology but still saving time in modern days just type PITC (space) your reference number and send it to 8334.

Checking MEPCO Bill Via App

Checking your bills through the internet on your mobile or a computer doesn’t fascinate you, so a bill checking app might be the best option for you. You can download the official app from the playstore and easily see your bill showing consumed units, due dates and payable amounts. Mostly these apps are completely free, your personal data secured and no registration is required to check your wapda bill.

MEPCO Bill Payment Methods

After that you’ve seen your MEPCO bill, duplicated a digital copy of your bill and saved it in the pdf format for your records and future reference. Then comes the important step, that is paying your bill and saving the receipts for proof that you’ve paid the bill. Conventional ways of going to banks waiting in queues or going to nearest mepco office to pay your bill still exist. But as the digital world is taking over the ways of checking your electricity bill, so does paying your bill. You can pay your bills through JazzCash, EasyPaisa, and internet banking like MCB, UBL and many more.

Payment at Digital banks

There are many payment options, including jazzcash, easypaisa, Upaisa, daraz wallet and other bank accounts. Open any of the apps that you like, navigate to pay bills online, choose mepco. Enter your 14-Digit reference number or consumer Id and pay the bill.

Payment at MEPCO Offices & Banks

Physically going to the mepco office and banks is also a way to pay your electricity bills. It’s the conventional way of doing it most people use it even in today’s day and age. It is mostly time consuming but after all you can pay your bills this way.

Paying MEPCO Bill via ATM Machines

Mepco bill can also be paid via thousands of ATM Machines around the country, you just need your 14-Digit consumer or 10-Digit Consumer ID. You will also get receipt from the ATM machine.

MEPCO Bill Installment

If you were unfortunate in paying your (MEPCO) bill from the above section due to any financial reason. Those involving very high bill due to peak hours consumption and never expecting the bills to be that high. That’s when, mepco bill installment comes in which basically means you can pay your bill in different parts at your ease. Below is the list of people who can help you in installment and the ranges upto what price range.

| Competent Authority | Installments of Bills |

| SDO / AM(O) Sub-Divisional Officer / Assistant Manager (Operation) | 03 Monthly InstallmentsMaximum bill amount: Up to Rs. 50,000 |

| RO / AM(CS) Revenue Officer / Assistant Manager (Customer Services) | 03 Monthly InstallmentsMaximum bill amount: Up to Rs. 50,000 |

| XEN / DM(O) Executive Engineer / Deputy Manager (Operation) | 03 Monthly InstallmentsMaximum bill amount: Up to Rs. 200,000 |

| SE / Manager (O) Superintending Engineer / Manager (Operation) | 04 Monthly InstallmentsMaximum bill amount: Up to Rs. 500,000 |

| Director Commercial | 05 Monthly InstallmentsMaximum bill amount: Up to Rs. 1,000,000 |

| CSD (Customer Services Director) | 12 Monthly InstallmentsMaximum bill amount: Up to Rs. 20 Million |

| CEO (Chief Executive Officer) | Maximum 10 Days ExtensionApplicable for all bill amounts |

Important Note: Bill installments are granted at the discretion of the competent authority and may depend on the consumer’s payment history, the reason for the request, and the applicable provisions of the MEPCO Consumer Service Manual. Supporting documents or a written application may be required before approval.

What is a MEPCO Bill?

So far we have discussed all about checking, duplicating, downloading your bill and briefly the consumed units and due date. But what more information does it have to offer you in first place. Furthermore, starting from consumer name, address, Reference number and consumer ID in the top section. In the middle left section you have consumed units and all the taxes from GST to FAP. Right middle section of the previous history of monthly bills that you received and their total consumed units. Lower section is for your information that what the payable amount is before the due date and after due date.

About MEPCO

So now as we have understood what mepco bill is, but what about MEPCO and its brief history. MEPCO was established on 14 May 1998 as the Government company to serve the people of South Punjab. Till this day in 2026 it still remains the biggest electricity distribution company serving more than 30 million consumers. Additionally, dealing with the duplicate bills, new connections and your complaints regarding any load shedding.

MEPCO is Multan Electric Power Company, a DISCO (Distribution Company) like LESCO, GEPCO, FESCO and many more. They are Affiliated with WAPDA (Water and Power Development Authority) and IPPs (Independent Power Producers). Furthermore, wapda and ipps are responsible for electricity production and transmission through DISCOS.

8+ Million

Consumers Served

13+

Districts Covered

Since 1998

Serving Punjab

What is WAPDA?

As previously discussed, WAPDA is water and power development authority owned by government and was established on 12 february 1958. Additionally, it is involved in managing the natural resources of pakistan like water in tarbela and mangla dam for electricity generation. Then this electricity through different grids and power lines is distributed to DISCOS and then to different households, shops, offices and agriculture.

Areas Under MEPCO

In the sections above we have discussed about how MEPCO is one of the largest DISCO (distribution company) supplied by WAPDA and regulated by NEPRA. NEPRA is National Electric Power Regulation Authority involved in licensing electricity generation, transmission, distribution and setting tariffs for electric power. However, MEPCO supplies 13 districts in South Punjab from Multan to Bahawalpur. Below is a list of Cities, Divisions and Disctricts covered by MEPCO.

| No. | MEPCO Division | District | Major Cities & Tehsils Covered |

| 1 | Multan Division | Multan | Multan City, Multan Saddar, Shujabad, Jalalpur Pirwala |

| 2 | Khanewal Division | Khanewal | Khanewal, Mian Channu, Kabirwala, Jahanian |

| 3 | Bahawalpur Division | Bahawalpur | Bahawalpur, Ahmadpur East, Hasilpur, Khairpur Tamewali, Yazman |

| 4 | Muzaffargarh Division | Muzaffargarh | Muzaffargarh, Alipur, Jatoi |

| 5 | Rahim Yar Khan Division | Rahim Yar Khan | Rahim Yar Khan, Sadiqabad, Khanpur, Liaquatpur |

| 6 | Vehari Division | Vehari | Vehari, Burewala, Mailsi |

| 7 | Dera Ghazi Khan Division | Dera Ghazi Khan | Dera Ghazi Khan, Taunsa Sharif, Kot Chutta, Koh-e-Suleman Region |

| 8 | Pakpattan Division | Pakpattan | Pakpattan, Arifwala |

| 9 | Lodhran Division | Lodhran | Lodhran, Dunyapur, Kehror Pacca |

| 10 | Layyah Division | Layyah | Layyah, Karor Lal Esan, Chaubara |

| 11 | Bahawalnagar Division | Bahawalnagar | Bahawalnagar, Chishtian, Haroonabad, Minchinabad, Fort Abbas |

| 12 | Kot Addu Division | Kot Addu | Kot Addu, Chowk Munda |

| 13 | Rajanpur Division | Rajanpur | Rajanpur, Jampur, Rojhan |

| 14 | Sahiwal Division | Sahiwal | Sahiwal, Chichawatni |

MEPCO Peak Hours

You may have come across times when you were expecting your bill to be 5000Pkr but it came about 10000Pkr, do you know why? That’s when understanding of peak hours makes sense to everyone. So, what are peak hours? – It’s the time when demand of electricity and usage both are high, also the tariff of the electricity peaks 2x. Additionally, instead of using the same amount of bijli units you get the different electricity bill. Also, it is a good approach to use minimum electricity during these hours, these range mostly from 6pm to 11pm in most cases.

MEPCO Meter Reading

Ever wondered how you get your wapda bill with accurate reading of your electricity units each month. Clearly, there is a team of MEPCO allocated different areas to read your electricity meters and take pictures and send them to their office. Then these units are subtracted from the previous reading to get the estimate of your current units of this month. In this way your units, current slab and tariff are calculated accordingly to provide you with the bill.

MEPCO Tariffs & Charges

Understand your electricity rates and additional charges that appear on your MEPCO bill.

Units / Category

Rate (PKR/Unit)

Description

| 1-100 | Rs. 10.54 | Protected consumers |

| 101-200 | Rs. 28.91 | Low consumption |

| 201-300 | Rs. 33.10 | Medium consumption |

| 301-700 | Rs. 42.62 | Standard consumption |

| 700+ | Rs. 47.69 | High consumption |

Units / Category

Rate (PKR/Unit)

Description

| Commercial | Rs. 45.43 | Protected consumers |

| General Services | Rs. 43.17 | Medium consumption |

| Time of Use | Rs. 43.17 | Depends on usage |

Units / Category

Rate (PKR/Unit)

Description

| B1 (Small) | Rs. 30.31 | Protected consumers |

| B2 (Medium) | Rs. 33.38 | Low consumption |

| B3 (Large) | Rs. 41.76 | Medium consumption |

How to Save Electricity and Reduce MEPCO Bill

In the previous sections we discussed how mepco works, peak hours and meter readings are collected. After all of this you are still getting bills that are out of comprehension, because you thought you consumed less units and you were in a perfect slab according to your usage. Well mostly this is not the case because your MEPCO bill depends upon many factors such as FAP (fuel adjustment prices), GST (Government Sales Tax) and Other taxes.

So, How to save electricity? There is no simple answer to that question, It all comes to using less electricity in many cases. In this time of inflating economy, sky high fuel prices, and scorching heat of summer it becomes impossible to use less units and maintaining your lowest slab. Going off grid, shifting most of your electricity load to solar and using new DC technologies using less wattage becomes the only reasonable alternative.

Turn off Unused Lights

Make it a habit to turn off lights when leaving a room. Small changes add up to big savings.

Use LED Bulbs

LED bulbs use 75% less energy than traditional incandescent bulbs and last 25 times longer.

Set AC to 26°C

Every degree lower increases energy consumption by 3-5%. 26°C is the sweet spot for comfort and savings.

Avoid Peak Hours

Run heavy appliances like washing machines during off-peak hours (11 AM – 5 PM) for lower rates.

MEPCO Management and Organization

| Need Help With? | Responsible Officer | Head Office Contact |

| Bill Corrections & Duplicate Bills | Chief Engineer (Customer Services) | 061-9220182 |

| Power Outages & Electricity Operations | General Manager (Operation) | 061-9220282 |

| Technical Faults & Distribution Network | Chief Engineer (O&M Distribution) | 061-9220168 |

| Recruitment & HR Matters | Director General (HR & Administration) | 061-9220267 |

| Financial Matters | Finance Director | 061-9220117 |

| Executive Office & General Administration | Chief Executive Officer (CEO) | 061-9220222 |

Note: The contact numbers above are for MEPCO Head Office departments. For local electricity faults, emergency complaints, or subdivision-level services, consumers should first contact their respective MEPCO subdivision or complaint center.

Frequently Asked Questions

Conclusion

So, here at meetyourbills.com you can easily Check your MEPCO online bill in just a few seconds. No more waiting for the mails to get delivered and panicking over the due dates or what if I miss my due date. Also, once you get the mail and then again waiting in long queues to pay the bills. We are here to solve all these problems, you just need a reference number or a consumer id and put either on this page and duplicate, download your bills in pdf format.

Popular MEPCO Guides

Instant Bill Access

Get your mepco bill in seconds.

Accurate Billing Info

Official MEPCO data.

Secure & Private

Your data stays safe.

Works on Mobile

Access anywhere, anytime.